What Darknet Markets Actually Look Like From the Inside

June 9, 2026

Across 53 darknet marketplaces actively observed between January and April 2026, DarkOwl collected new listings spanning more than 3,200 unique category labels. That fragmentation is not an accident — markets and vendors invent categories independently, which means a listing for methamphetamine might be filed under “Stimulants,” “RC Chems,” “Speed,” “Uppers,” or something else entirely depending on where it’s posted.

Making sense of that data requires moving past the labels. Rather than treating market-defined categories as meaningful, DarkOwl normalizes every listing into a consistent framework, then aggregates those normalized categories to produce a fingerprint: a profile of what a market actually hosts, expressed as a distribution across standardized categories.

When you compare those fingerprints across the 53 markets active in Q1 2026, five structural groupings emerge. Below, we take a look at these findings.

Five Kinds of Darknet Markets

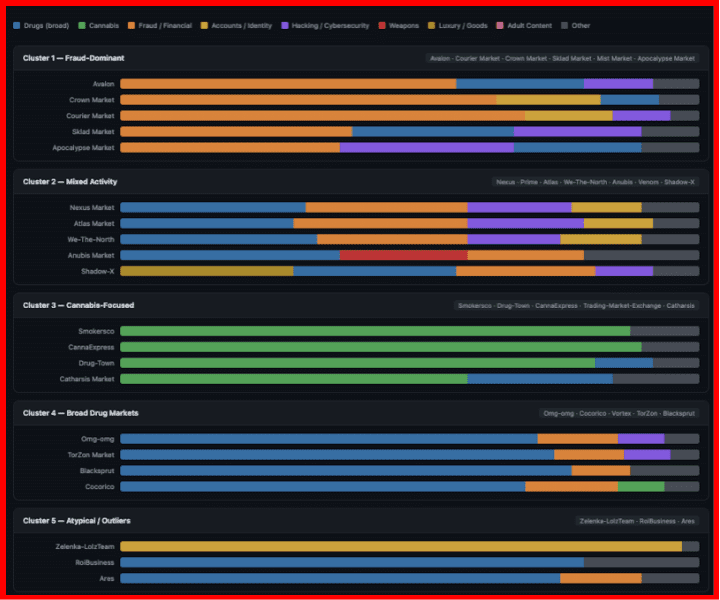

First Cluster: Fraud-Dominant Markets

Avalon, Crown Market, and Courier Market group together because financial fraud, identity documents, and stolen credentials dominate their listing mix — not drugs. Sklad Market, Mist Market, and Apocalypse Market form a related sub-cluster, where fraud remains primary but is accompanied by a substantial hacking and cybersecurity presence. None of these markets are necessarily known by reputation as fraud platforms, but their listing distributions are unambiguous.

Second Cluster: Mixed-Activity Markets

Nexus Market, Atlas Market, Prime, and We-The-North maintain roughly balanced distributions across drugs, fraud, hacking tools, and compromised accounts. No single category dominates. Shadow-X occupies this cluster but stands out within it — it carries a notable share of luxury goods that distinguishes its profile from its peers. Anubis Market and Venom are grouped nearby, differentiated by a higher concentration of weapons listings alongside drugs.

Third Cluster: Cannabis-Focused Markets

Smokersco, CannaExpress, Drug-Town, and Trading-Market-Exchange group together not because they’re small or inactive but because their category distributions are so concentrated. These platforms sell almost exclusively cannabis — sometimes 85–90% of all listings fall into a single subcategory. Fingerprinting separates them from the broader drug markets precisely because their specialization is so pronounced. A platform that’s 90% cannabis looks nothing like a platform that’s 70% drugs across stimulants, opioids, psychedelics, and other classes.

Fourth Cluster: Broad Drug Markets

Omg-omg, TorZon, Blacksprut, Cocorico, and Vortex Market group here — drug listings dominate at 70–80%, with fraud and hacking as secondary categories. These are the markets the ecosystem knows by reputation, and their fingerprints confirm it.

Fifth Cluster: Atypical Outliers

Zelenka-LolzTeam hosts almost nothing but gaming accounts and social media profiles — its fingerprint bears no resemblance to any other market in the dataset. RoiBusiness and Ares are drug-focused but have low enough listing volumes that they remain separate from the main drug cluster, making cross-market comparison unreliable without accounting for scale.

Markets Don’t Stay Still

The cluster analysis reflects a four-month average, which obscures something important: several markets changed their category composition significantly over the period. Some changes are consistent with normal variation — different vendors posting different volumes in different months. Others are not.

Stargate Market is the clearest example. January listings are dominated by adult content — the platform looks, at first glance, like a niche adult market. By February the adult content has largely disappeared, replaced by drugs and fraud. March shifts again to cannabis and services. By April, financial accounts, identity fraud, and hacking tools dominate, and drug listings have almost vanished. Over four months, Stargate cycled through four structurally different profiles.

Avalon shows a different trajectory. January is drug-dominant. February brings a sharp increase in fraud. March sees reduced volume with a higher proportion of hacking and cybersecurity. By April, volume is significantly lower, and remaining listings are primarily fraud. The arc is consistent with a platform losing its drug vendor base — through enforcement action, vendor migration, or market reputation decline — with fraud listings filling the remaining activity.

Shadow-X begins the period with a distinctive luxury goods presence that places it as an outlier within the mixed cluster. That distinguishing feature disappears by April, replaced by the drugs-and-fraud profile that characterizes most of its neighbors. Whatever made Shadow-X distinctive in January was gone by Q2.

DarkHub shows the opposite pattern: category composition stays relatively consistent across all four months, but listing volume drops sharply in March and April. The mix doesn’t change — drugs and fraud, roughly stable proportions — but the platform is generating far fewer new listings. That’s a different kind of signal: not a change in what’s being sold, but a contraction in who’s selling it.

What this Means for Tracking Markets

Market reputation — what a platform is known for in forums, reviews, or community discussion — is a lagging and often inaccurate indicator of what’s actually being sold. Avalon does not carry a reputation as a fraud market. Its January data wouldn’t suggest one. Its April data is almost entirely fraud. An investigator relying on reputation-based targeting would have the wrong picture of Avalon for much of the year.

The cluster analysis and temporal tracking together point toward a more reliable approach: compare what a market is really hosting, using normalized categories, against the broader ecosystem. Markets that appear structurally similar to known fraud-dominant platforms are worth treating as fraud-dominant platforms, regardless of what they’re called or how they’re marketed. Markets whose category composition is shifting toward fraud or hacking-focused activity are worth monitoring more closely, because that shift is often a precursor to vendor migration, enforcement attention, or platform collapse.

When a market does collapse — as happens regularly in darknet ecosystems — its vendor population redistributes. Fingerprinting the collapsed market makes it possible to track that redistribution: look for increases in specific category clusters on other active platforms in the weeks following shutdown. The category signal persists after the market name disappears.

Analysis based on DarkOwl’s DarkMart dataset, covering 53 active markets and new listings observed from January through April 2026. Category distributions are derived from DarkOwl’s normalized category framework, applied uniformly across all markets including listings without market-defined categories.

Curious how DarkOwl can do deeper analysis for your company? Contact us.