Darknet Market Vendor Analysis

What vendor behavior actually looks like across 7,314 sellers — and why the same name on eleven markets doesn’t mean what you’d expect.

June 03, 2026

Of the 7,314 vendors active on darknet markets between January and April 2026, more than 2,000 posted exactly one listing. Another 1,000+ posted only two. The distribution has a long tail: the vast majority of accounts are transient, low-volume, and individually uninformative. They appear and disappear without accumulating enough activity to characterize.

This is the baseline condition of darknet vendor data. Most of it is noise. What’s operationally useful is concentrated in a smaller population of high-activity sellers whose behavior is sustained enough to analyze — and whose patterns persist across migrations, rebranding, and platform shifts.

Among the 285 vendors who posted more than 50 new listings during the period, two findings stand out.

Drug Vendors Specialize. Fraud Vendors Diversify.

The first finding is about specialization. Drug vendors, in aggregate, are more narrowly focused than any other vendor category. Cannabis sellers are the extreme case: most concentrate 90% or more of their activity in cannabis listings, with almost nothing else. Stimulant specialists and opioid specialists are nearly as concentrated — a vendor who sells stimulants rarely sells psychedelics or opioids at meaningful volume, even within the broader drug category.

This pattern is analytically useful. A cannabis vendor with 200 listings is maximally exposed in a single product category. Their profile is easy to recognize, easy to track across platforms, and easy to distinguish from vendors who happen to have a few cannabis listings alongside other inventory.

Broad-spectrum drug vendors — those distributing activity across stimulants, opioids, psychedelics, and other subcategories — exist but are less common. When they appear, the diversity itself is a signal. Vendors who source across multiple drug classes typically operate at larger scale or have more diversified supply chains than single-substance specialists.

Fraud vendors look structurally different. The typical high-activity fraud vendor spreads across financial instruments, identity documents, compromised accounts, and sometimes hacking tools within the same portfolio. This breadth is consistent with organized operations that source across multiple pipelines — not a single individual with a specific product, but a coordinated set of supply relationships. An investigator treating a fraud vendor the same way as a drug vendor — looking for a narrow category concentration — will misread the profile.

The Username Problem

The second finding concerns identity. Darknet vendors routinely reuse usernames across platforms, and other vendors independently register identical names on markets where those names aren’t taken. The result is that a username, on its own, is an ambiguous identifier.

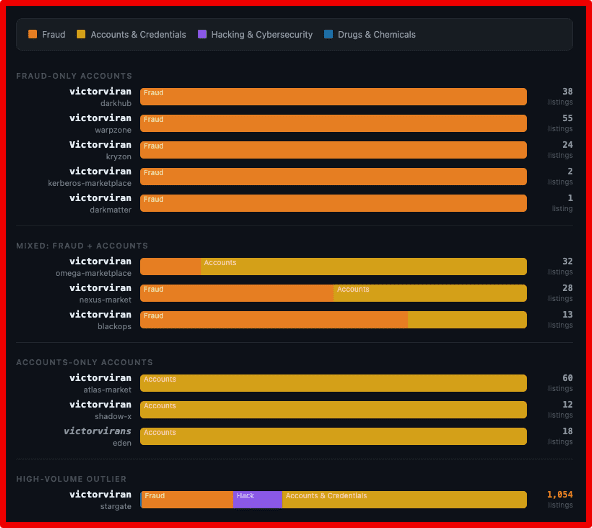

The username victorviran appears on eleven markets during the January–April period. It’s an instructive example because the behavioral divergence across those eleven accounts is stark.

Three of the accounts — on WarpZone, Atlas Market, and Nexus Market — show nearly identical fingerprints: almost entirely accounts and credentials, with minimal activity in other categories. The structural similarity across platforms is too close to be coincidental. These accounts are plausibly the same operator maintaining parallel presence on multiple markets. The Stargate account bearing the same name has expanded its profile to include hacking tools alongside credentials — either an evolution of the same operation or a closely related actor.

Then there are accounts with the same name selling primarily financial fraud, with no meaningful overlap with the credentials-focused accounts. And at least one victorviran account whose listings are drugs. The profile bears no resemblance to the others.

The inverse of this problem is equally significant, and in some ways more useful to investigators. Different vendors operating under different names can produce nearly identical fingerprints — the same category distribution, the same subcategory emphasis, similar listing volumes. When a vendor migrates from a collapsed market to a new platform under a new username, the fingerprint often follows.

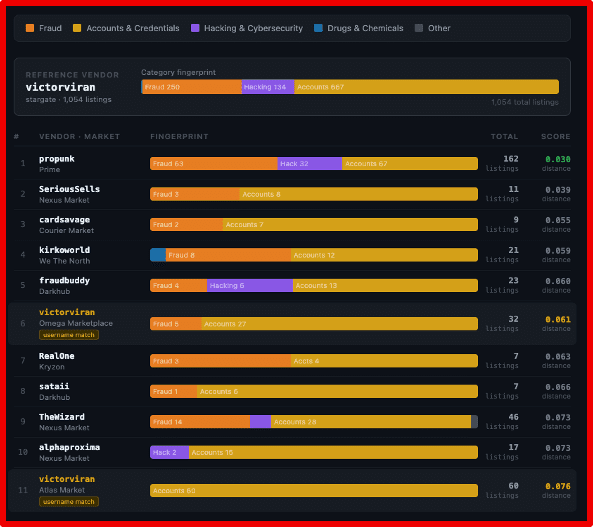

This is where similarity search across markets becomes operationally relevant. Starting from a known vendor profile — say, a confirmed drug distributor on a market that has since shut down — you can compute fingerprint similarity across all vendors on currently active markets and surface accounts whose behavioral profiles closely match. The name is different. The behavior is not.

In the victorviran similarity network, the most closely matching profiles include accounts that share the username. But they also include accounts that don’t. The fingerprint search finds both, and the username search alone would miss the latter entirely.

What Vendor Fingerprints Actually Tell You

The operational framing matters here. Fingerprints are a similarity signal, not an attribution mechanism. Two vendors with identical category distributions are not necessarily the same person. But vendors with highly similar fingerprints, appearing on different platforms in overlapping time windows, are worth treating as related until evidence suggests otherwise. The alternative — treating every new username as a new actor — understates continuity in an ecosystem where continuity is deliberately obscured.

The specialization patterns matter too. A vendor who is 95% cannabis is not a general drug distributor who happens to sell cannabis. They’re a cannabis-specific operator, and their investigative profile should reflect that. A fraud vendor who combines identity documents, financial instruments, and hacking tools in a single portfolio is not an opportunistic individual seller — the breadth implies supply chain access that a single person doesn’t typically have.

Seven thousand vendors is too many to work through manually. Fingerprint-based clustering reduces that population to meaningful groups: the cannabis specialists who cluster together by behavior, the credentials vendors who look similar across platforms, the broad-spectrum fraud operations that stand apart from everything else. The 285 high-activity vendors are not representative of the 7,314 — they’re a different kind of actor and analyzing them as a separate population surfaces patterns that the full dataset obscures.

Analysis based on DarkOwl’s DarkMart dataset, covering 7,314 active vendors across 53 markets from January through April 2026. Vendor fingerprints are derived from normalized category distributions across all listings associated with each vendor during the period. High-activity vendors are defined as those with 50 or more new listings during the observation window.

Curious to learn more about dark web monitoring? Contact us.